Andy Sena Agbley

sirandy13@gmail.com

Introduction

Over the past two decades, Ghana’s financial sector has undergone significant transformation. This period has been marked by liberalization, rapid expansion, consolidation, improved customer service, and technological innovation. These developments have been driven by key legislative reforms such as the Bank of Ghana Act (2002), Banking Act (2004), and the Foreign Exchange Act (2006). These laws aimed to liberalize the sector, strengthen regulatory frameworks, and promote competition. However, despite these advancements, a persistent and concerning trend has emerged: the financial sector continues to prioritize commerce and services at the expense of Ghana’s real sector – namely agriculture, manufacturing, and infrastructure. The sector has also faced major challenges, most notably the GHS 25 billion financial sector clean-up between 2017 and 2019, which led to the revocation of licenses and consolidation of several banks. While these measures stabilized the industry, they also highlighted deep-rooted issues such as poor corporate governance and insufficient capitalization. A closer examination of lending patterns and global benchmarks reveals a structurally risk-averse banking sector, largely disinterested in driving long-term national productivity, the real sector of the economy.

Here, I define the real sector of an economy as that part of the economy that entails manufacturing, construction, processing and production of goods without the service. In this definition, I consider mining, construction (real estate and roads infrastructure), manufacturing, commercial farming, commercial fishing, commercial livestock farming, processing of agriculture product.

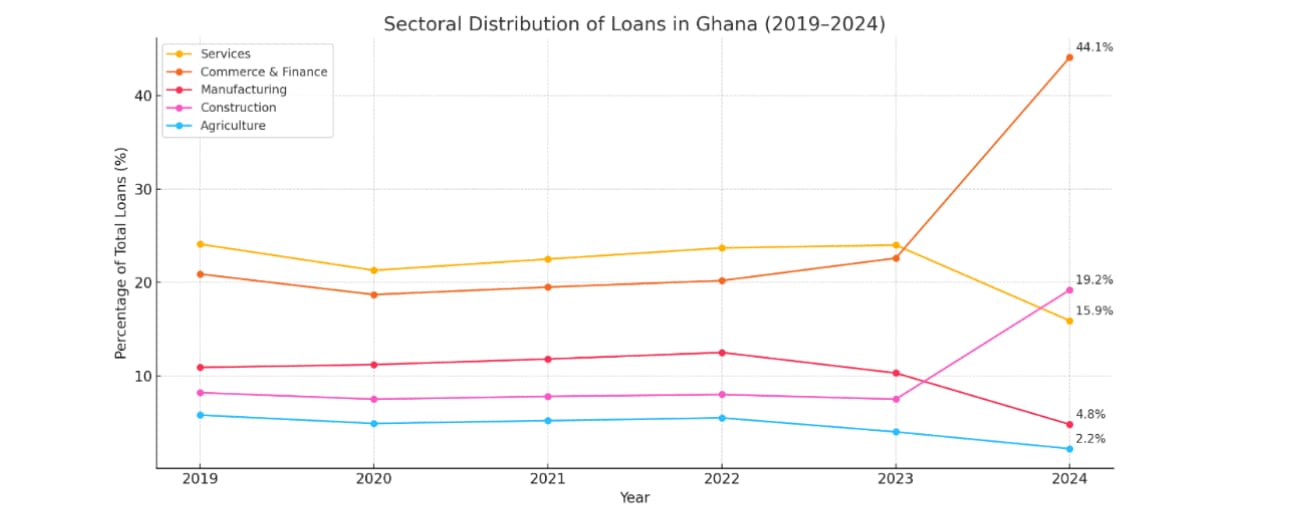

Lending Patterns, a Tilt towards Commerce

An analysis of the financial service sector, by examining the published financial report of banks in Ghana, show a lack of commitment by the banks towards the real sector of the economy per the definition above. An analysis of lending pattern from 2019 to 2024 reveals a significant bias towards commerce and finance. In 2024 alone, loans to these sectors surged to 44.1% of total lending. In contrast, agriculture and manufacturing received only 2.2% and 4.8%, respectively.

| Year | Services | Commerce & Finance | Manufacturing | Construction | Agriculture |

| 2019 | 24.1% | 20.9% | 10.9% | 8.2% | 5.8% |

| 2020 | 21.3% | 18.7% | 11.2% | 7.5% | 4.9% |

| 2021 | 22.5% | 19.5% | 11.8% | 7.8% | 5.2% |

| 2022 | 23.7% | 20.2% | 12.5% | 8.0% | 5.5% |

| 2023 | 24.0% | 22.6% | 10.3% | 7.5% | 4.0% |

| 2024 | 15.9% | 44.1% | 4.8% | 19.2% | 2.2% |

Analysis:

→ Commerce & Finance loans more than doubled between 2022 and 2024—from 20.2% to 44.1%.

→ Manufacturing saw a steep decline from 12.5% (2022) to 4.8% (2024).

→ Agriculture dropped to just 2.2%, despite employing over 30% of the population and the GIRSAL initiative.

Such lending patterns raise alarms about the underfunding of critical sectors like agriculture and manufacturing. These sectors are crucial for food security, employment, and industrialization. Banks’ aversion to long-term risk is preventing investments in areas with potential to transform the economy of Ghana, curb inflation whiles stabilizing the local currency.

The Cost of Capital: A Barrier to Real Sector Growth

High-interest rates further exacerbate the difficulties faced by the real sector. As of May 2025, the Bank of Ghana’s policy rate stood at 28.0%, while commercial lending rates ranged between 20% and 50%. In contrast, Banks in China and those in the Eurozone maintain significantly lower rates, providing a competitive edge to their domestic industries. This disparity explains why foreign firms are able to invest in capital-intensive sectors in Ghana, while local entrepreneurs remain confined to commerce and services. A comparative table below illustrates how prohibitive Ghana’s lending rates are, especially for sectors like agriculture and manufacturing, when benchmarked against China (Asia) and the Eurozone.

| Region | Benchmark Rate | Mortgage Loans | Consumer Loans | Industry Loans | Agriculture Loans |

| China | 3.10% | 3.60% | ≥3.00% | ~3.10–3.60% | Below 3.10% |

| Eurozone | 4.08% | ~3.32% | ~7.58% | ~3.67–4.10% | ~3.67–4.10% |

| Ghana | ~30.25% | 20–50% | 20–50% | 30–50% | 30–50% |

Analysis:

→ Ghana’s interest rates are 8–10x higher than global peer countries.

→ Agriculture loans in China cost under 3.1%; in Ghana, they may exceed 50%.

→ These rates make investment in long-term projects (like agro-processing, commercial farming, or manufacturing) near impossible for local entrepreneurs.

This disparity in interest rates places Ghanaian entrepreneurs at a disadvantage, particularly in capital-intensive sectors like agriculture and manufacturing. The high cost of borrowing discourages investment in these areas, leading to reliance on imports and hindering the country’s industrialization efforts. The banks in Ghana find it more profitable to invest heavily in the government of Ghana’s financial instruments, like the Bonds and treasury bills, overlooking the real returns that await them should they commit to long-term financing of the real sectors of the economy.

The Role of Development Banks and Policy Coordination

Ghana’s development banks, NIB, DBG, ADB, Exim Bank, GCB, and GIRSAL are critical to financing strategic sectors. However, their potential is limited by poor capitalization, governance issues, and lack of coordination with key ministries such as Finance, Agriculture, Trade & Industry, and Transport. Strengthening these banks and aligning their mandates with national development goals is essential if Ghana is to see a significant structural change that will anchor low inflation and stable currency.

The Consequence: Foreign Dominance of the Real Sector

The attainment of economic sovereignty lies in what percentage of control the government and it citizens have over the production and distribution of goods and service in a country, it is for this and many reasons, this writer for instance was dissatisfied with the approach adopted in the clean-up of the financial service sector between 2017 to 2019. About 90% of all the financial institutions, which collapsed or ceased to operate, were wholly own by Ghanaians. Today, the financial service sector of Ghana is highly dominated by foreign-backed institutions. Such a classical nature of the financial service sector is prevalent in virtually all sectors of the Ghanaian economy. In the real sector, the lack of access to affordable financing for Ghanaian businesses in agriculture, mining, and industry has led to outsized control by foreign entities.

Foreign companies dominate key sectors:

• Tropo Farms Ltd (German) – Largest fish farm

• De Heus Ghana (Dutch) – Leading feed processor

• Golden Exotic (French) – Largest banana plantation

• B5 Plus Ltd (Indian) – Major steel manufacturer

• Newmont Ghana (American) – Largest mining firm

• Melcom & China Mall (India & China) – Leading retail outlets

None of these companies got their funding or start-up support from any bank in Ghana, these foreign enterprises often secure financing from their home countries at lower interest rates, enabling them to invest heavily in Ghana’s economy while Ghanaian banks merely facilitate their profit repatriation. Meanwhile, local entrepreneurs struggle to access affordable capital, limiting their participation in these lucrative sectors of the economy. The repatriation of this returns or profit from their investment significantly affects the local currency.

Lazy Banking and Profit Extraction

Ghanaian banks, while claiming operational risk aversion, are engaged in what some observers describe as “lazy banking”. Heavy lending to importers, traders, and consumer credit, buying of T-Bills, multiple fees for basic services: ATM withdrawals, mobile apps, statement requests, cheque clearance, inter-accounts transfers (Bank to MOMO) and avoiding long-term developmental risk, the very lifeline for transforming the economy.

Contrary to the lack of interest by the banks in the real sectors of the economy, their participation and support for those sectors would spare essential value addition for export, reducing dependency on imports, job creation, and improving food security. Underfunding local production inflates import bills and depletes forex reserves, further weakening the cedi. A services and commerce heavy economy cannot absorb the labour force entering the market annually, driving poverty and insecurity, but with the new government policy of a 24-hour economy, the expectation is that the real sectors would see significant gain through a policy shift by the banks towards the real sectors of the economy.

Initiatives and the Path Forward

Recognizing these issues, the government and financial institutions launched the GIRSAL (Ghana Incentive-Based Risk-Sharing System for Agricultural Lending): Designed to de-risk agricultural loans. So far, GIRSAL has engaged 35 financial institutions and guaranteed GHS 1.49 billion in loans, benefiting 146 agribusinesses across 76 districts as at January 2024 with over GHS 502.36 M worth of guarantees loans successfully repaid, representing 33.72% with the rest expected. However, these efforts should be scaled-up for full implementation, and supported by a fundamental shift in banking culture.

This writer is of the firm believe that the case of Ghana is not a lost one, taking a cue from Cocoa Bills Exchange Programme, which led to the issuance of new Cocoa Bonds, allows holders of short-term debt securities (Cocoa Bills) to exchange them for longer-term debt securities (Cocoa Bonds). This can be transformed into a broader Agriculture, Infrastructure, and Industrial Bonds, leveraging on the long-term funding nature of bonds, thus making long-term funding available for Ghanaian entrepreneurs who are willing to venture into the real sectors of the economy. This bond ingenuity would meaningfully attract institutional investors, like pension and insurance funds, seeking long-term returns, thereby channeling capital into productive sectors.

Targeted Credit Strategies

Many successful economies use policy banks and concessional lending to drive industrialization. For example:

→ Japan and South Korea: Used state-backed banks to direct credit to key industries.

→ Brazil and India: Offer concessional rates to small and medium enterprises.

Ghana must adopt similar strategies or bond initiatives suggested above if it is to realize the goals of paradigm shift in economic structure and the 24-hour economy’s full realization.

Policy Recommendations

→ Develop a national credit policy: Align lending with economic goals.

→ Cap rates for targeted sectors: Introduce interest rate ceilings for agriculture and manufacturing.

→ Capitalize development banks: Equip NIB, DBG, Exim Bank, ADB, and GIRSAL to serve strategic sectors.

→ Encourage patient capital: Promote long-term, low-cost financing (Bonds).

→ Enhance coordination: Synchronize financial policy with agriculture, trade, and infrastructure plans.

Conclusion

Ghana’s banking sector holds the keys to the transformation of Ghana’s real sector, but only if it chooses to unlock that potential. While significant strides have been made in reforming and stabilizing the financial system, there remains a critical need to realign banking practices with the country’s developmental objectives. The current trend of prioritizing commerce over production is a strategic errorwith long-term consequences. Reversing this trajectory will require not just reforms, but a complete paradigm shift in banking philosophy: from short-term profit to national development objectives, aligning with the aspiration of the country Ghana. By prioritizing lending to the real sector, reducing interest rates, and supporting local entrepreneurs, Ghana can foster a more inclusive and resilient economy.